Stock Research – “The Puppet Show Nobody asked for and we Don’t Know we’re Watching”

Recently at an event, I was schmoozing and had the ‘what do you do for work?’ question came up.

I said I’m a Wealth Advisor, was at the bank for 10 years then started Clarify Wealth last year.

‘Independent firm eh, so now that you’re on your own – where do you get your research?’ he asked.

‘What kind of research are you referring to?’

‘Well, my guy at [Bank Brokerage] has a team of people, I’m in retirement now so they pick dividend stocks, and they send me the research on the companies.’

Biting my tongue: ‘Is the research right?’

He chuckled, ‘sometimes yes, sometimes no.’

Let’s talk about research.

If the ‘greatest trick the devil ever pulled was convincing the world he didn’t exist’ – then the greatest trick in Stock Broker Land is convincing the world that investment research is an unbiased, accurate, and valuable to the end user… and not just Wall Street’s Puppet Show.

Is it accurate?

Unbiased,

And is there any value to those who use it.

Here’s how research works in Stock Broker Land:

Stock research was (and still is?) a tool advisors at big firms would have access to for their own purposes and share with their clients. It’s one of the selling features of being with a big firm – that the have a capital markets division, filled with expert analysts who know the companies they study inside and out – which ideally makes the advisors pick better portfolios, and clients get better returns.

The finger is on the pulse they say – ‘and this is a good thing’.

That’s essentially the pitch. Our group, out of all the investment researchers in the world doing the same thing is different, and has solved capital markets.

The idea being that the advisor is putting clients into superior portfolios, and the client can then walk away thinking they’ve just made a good decision with their money.

The reality couldn’t be further from the truth.

This industry has a problem with selling people on the idea of short-term investing strategies masquerading as wealth enhancing.

The research arms of brokerages are a marketing department in disguise, busy-work with a brand behind it.

How they work:

They’re essentially ‘cheat sheets’ for advisors who still pick stocks to use when a client calls them up asking about Acme Co.

“It’s a buy, our analysts are seeing a 12 month return of __%, and the dividend yield is __%, [insert a few bullet points of the comings and goings of the company found on the report], and the analyst ranks it a ‘buy’, of course, I like it too”.

If you look at stock ratings, or what the analysts at various brokerage houses are saying in research reports you’ll notice a trend – most stocks are rated some form of ‘hold’, ‘buy’ or ‘action list buy’ … rarely is there a ‘sell’ recommendation before it is too late.

A problem lies in the playground of Stock Broker Land, nobody wants to offend anyone – and with good reason.

Investment banking brings in huge fee revenue for the banks.

Any time a company wants to issue stock, debt, preferred shares, or advise on mergers and acquisitions, they use the investment banking.

It’s a huge profit centre for the banks.

In the Brokerage Land playground – they know that any company needing their services is going to be looking for friendly banks – the kind that like their business and are supportive… so calling their stock a ‘sell’ isn’t going to win many favours.

“If you don’t have anything nice to say, don’t say it at all.”

But this is supposed to be research, unbiased and backed by thorough analysis, right? Some sort of Scientific process?

This creates a magnet next to a compass situation where the one holding it can clearly see where north is – but the ‘you know what would be better for our company – if you could just bring it over here a little bit’ culture persists.

Clients aren’t supposed to see this.

John and Jane who are busy raising their kids, answering work emails at night, and saving for retirement… they are supposed to see the hold rating at face value and feel good about what they’re investing in.

The mucky questions, like ‘is this even legitimate research?’ are secondary.

Defenders of the stock research reports will say ‘so what if the ratings are skewed, just call a hold a sell, buy really means hold, and action list buy means just a buy – learn the customs and advise accordingly – there’s still good stuff in these reports.’

Is there though?

Is there any evidence to show that these reports are anything but a façade or puppet show to make brokers look like there is something valuable in them when it’s not just ‘busy work’ but actually detrimental?

This excerpt from Daniel Crosby’s hit ‘The Laws of Wealth: Psychology and the Secret to Investing Success’ which tackles that topic:

“…David Dreman found that most (59%) of Wall Street ‘consensus’ forecasts miss their targets by gaps so large as to make the results unusable – either under or overshooting the actual number by more than 15%. Further analysis by Dreman found that from 1973 to 1993, the nearly 80,000 estimates he looked at had a mere 1 in 170 chance of being within 5% of the actual number.”

For context, a broken clock is right 1/720 times per day (1,440 for those using the 24-hour clock), so stock forecasts are only 4x more likely to be within 5% using Dreman’s findings about brokerage reports than a broken clock showing the correct minute at any time during the day.

Well done.

When we compare these results with SPIVA – which has an annual report comparing active managers – those professional money managers who would use brokerage reports along with their own research to manage investment portfolios themselves, we see that it rarely turns into worthwhile results at all.

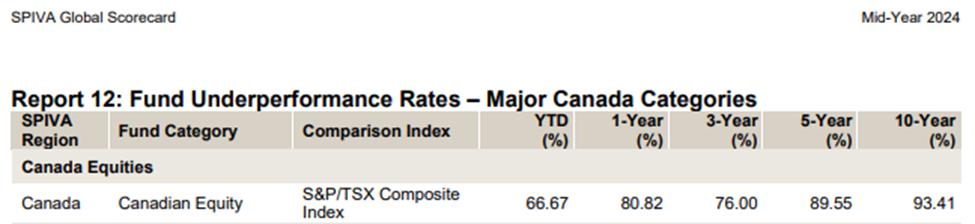

In Canada, 76% of managers underperformed the S&P/TSX over a 3 year period, this increases to 93.41% over a 10 year period.

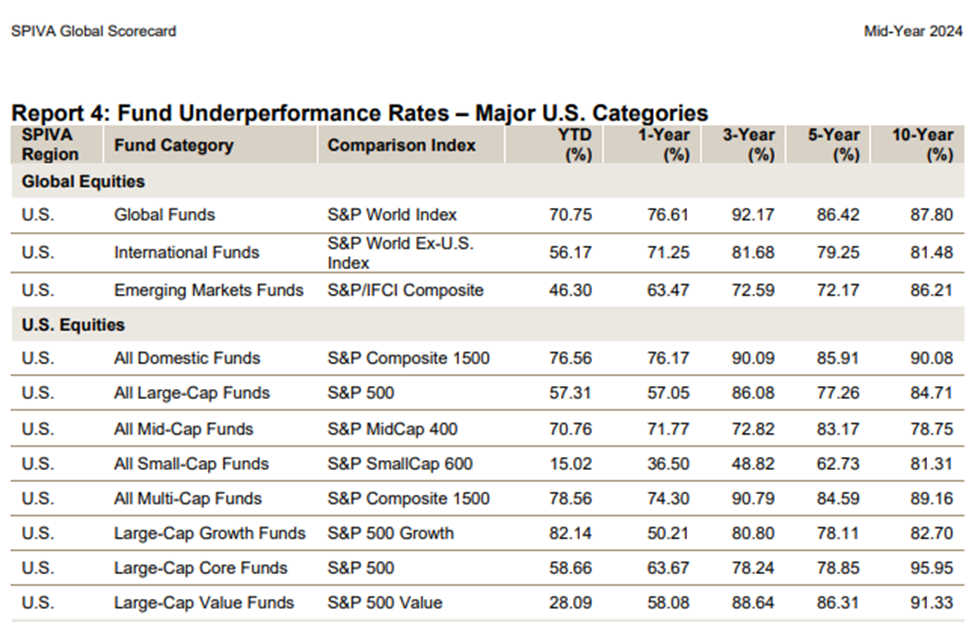

These results are consistent throughout the world with the US….

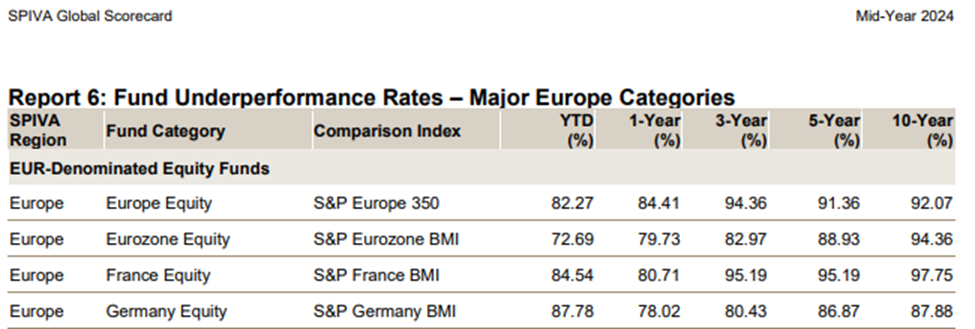

Europe…

Australia…

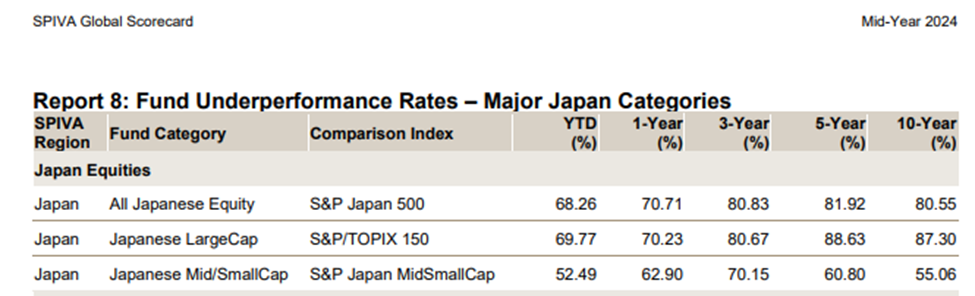

..and Japan all showing similar statistics. Click here for the SPIVA hub page where you can see the interactive chart, and also search for the reports.

You might be thinking: “So what if most underperformed, just pick the good ones that have performed well in the past”

Even those that have outperformed in the past show no more likelihood of continuing to outperform in the future.

SPIVA also has a persistence scorecard – studying how funds formerly in the top quartile fare in subsequent years.

“Among US top-quartile funds within all reported active domestic equity categories as of December 2019, not a single fund remained in the top quartile over the next four years.”

“The percentage of top-half actively managed domestic equity funds consistently remaining in the top half over a five-year period was less than a random distribution would suggest, evidence that active outperformance, when it occurs, tends to be the result of luck rather than genuine skill”

The common thread is that over time, fewer and fewer active managers are able to outperform their benchmarks.

This means that the presumed users of this information aren’t turning it into anything with value added results for the end investor.

So, what are stock research reports then?

Are they anything more than a puppet show to keep people entertained?

Given the research about these reports, what’s the point? And is the end investor better or worse off?

So how do I get my research now that I’m independent from the bank? The first step is to decide what is ‘research’ and what is not.

Discussion