I would wager that few personal finance influencers and professionals would answer the question above in the affirmative.

But should we look at personal debt as a consequence of public policy rather than simply a result of bad choices made by an individual.

In April, I attended a conference and workshop hosted by the Observatoire québécois des inégalités. One researcher, Émilie Laurin-Dansereau presented her analysis on the causes and consequences of higher levels of debt in society.

What are the causes of higher debt?

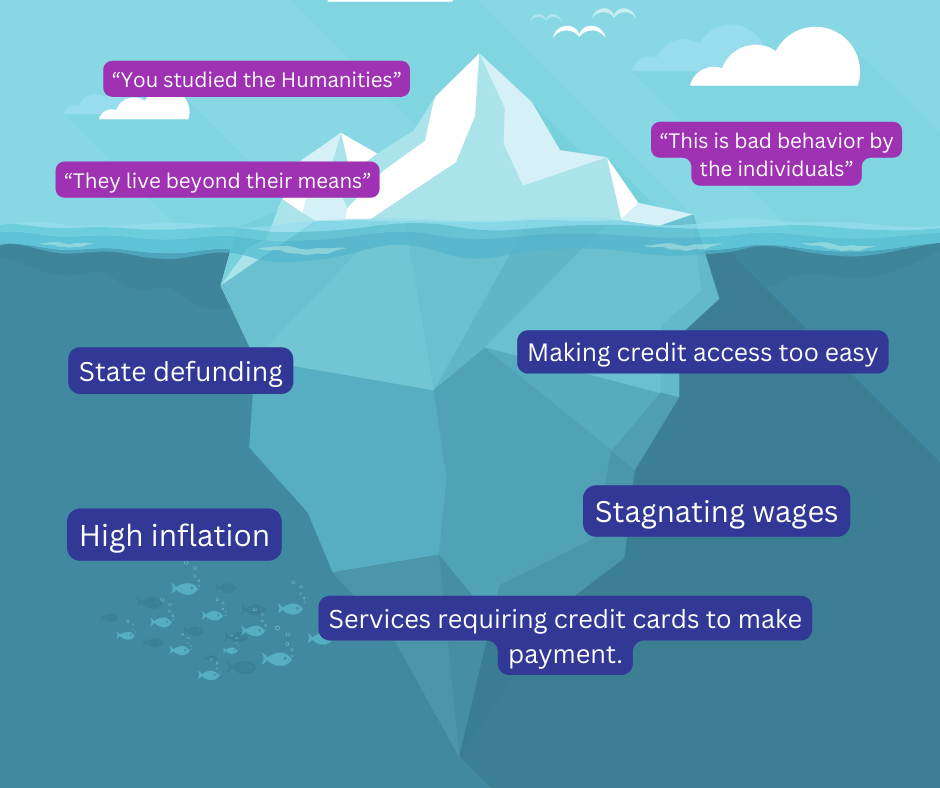

1️⃣ STAGNATING WAGES AND INFLATION:

Real wages have stagnated or even declined in many areas. Meanwhile, the cost of living, including essentials like housing, healthcare, education, and food, continues to rise. This divergence creates a situation where households increasingly struggle to make ends meet, pushing them to rely on credit to bridge the gap between their income and daily needs.

2️⃣ STATE DISENGAGEMENT:

With cuts to public services such as healthcare, education, and social services, citizens are forced to pay out of pocket for services that were once subsidized or free. For example, access to higher education is becoming increasingly expensive, pushing students to incur heavy debt to finance their studies. This trend of state disengagement can also exacerbate inequalities, with the most disadvantaged households being the hardest hit.

3️⃣ EASY ACCESS TO CREDIT:

Access to credit has become simpler with the rise of credit cards and personal loans, often offered with attractive short-term conditions but which can lead to high-interest rates in the long term.Moreover, some companies require the use of credit cards for essential transactions, such as paying utility bills or purchasing necessities. This phenomenon pushes consumers into debt to cover everyday expenses.

What are the potential consequences?

SURVEILLANCE and DISCRIMINATION:

The credit report, although intended to assess a person's financial capacity, is often used for purposes beyond this evaluation.

For instance, landlords frequently use these reports to judge the reliability of a potential tenant. However, a credit report provides no information about a tenant's behavior but rather about their debt repayment history.

This can lead to situations where people are unfairly discriminated against based on their credit report, perpetuating cycles of poverty and exclusion.

SOCIAL CONTROL and DEPENDENCE:

Credit thus becomes a means of social control, where individuals are judged and categorized based on their financial history. This dependence on credit can make individuals more vulnerable to economic fluctuations and financial crises.

Moreover, the fact that credit is necessary to access basic services helps to keep people in a state of permanent dependence, limiting their economic and personal freedom.

PSYCHOLOGICAL and SOCIAL IMPACTS:

The stress associated with chronic debt can have serious consequences for mental health, increasing levels of anxiety and depression. Socially, debt can also stigmatize individuals, preventing them from fully participating in society due to shame or fear of being judged.

Conclusion

The impact of too much debt can have grave consequences on society. Where as a society and as professionals in personal finance we decide to draw the line of between personal responsibility and public policy is a question that needs to be debated.

Feel free to tell us what you think.

Discussion