Insurance Disciplinary Decisions

Last week, I was working on a side project, and spent an unhealthy amount of time perusing the Insurance Council of BC’s Disciplinary Decisions site.

Last week, I was working on a side project, and spent an unhealthy amount of time perusing the Insurance Council of BC’s Disciplinary Decisions site. The Insurance Council of BC (I’m going to abbreviate it from now on as ICBC, even though I know BC folks will read that as Insurance Corporation of British Columbia, that province’s default auto insurer) has been relatively progressive in terms of regulating insurance practices, within the scope of its limitations.

It is common advice that consumers should explore the disciplinary history of a prospective financial advisor before working with that person, as indicated in this article from a prominent financial journalist.

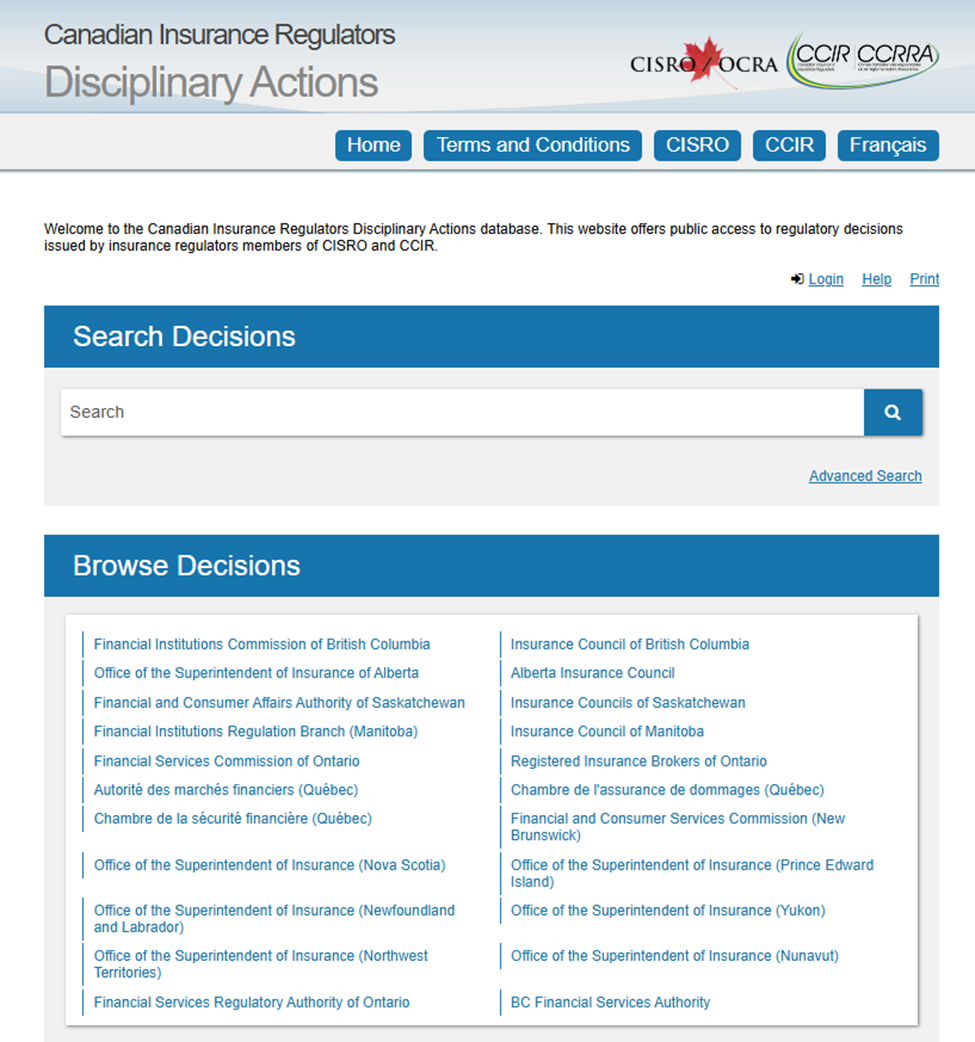

All thirteen provinces and territories participate in the Canadian Insurance Regulators Disciplinary Actions database. Decisions levied in the past 6 years or so, and any new decisions, should be searchable here.

What sorts of things do we find? Most decisions are related to one of two items:

1. Failure to comply with continuing education requirements. Alberta is the province where we’re least likely to see this infraction, as agents must attest to having completed courses which are pre-approved by the Alberta Accreditation Committee. Ontario operates on a near free-for-all basis, where agents are largely left to their own devices and expected to demonstrate that they have followed the rules. This leads to many more disciplinary infractions in that province.

2. Failure to renew errors and omissions insurance. While the requirements vary slightly from jurisdiction to jurisdiction, the majority of independent agents are required to carry E&O insurance. It’s a very common oversight, apparently, for agents to fail to renew their E&O insurance.

These two sources of disciplinary infractions are easily avoided. A consumer who finds an agent listed for this reason may find themselves dealing with somebody who isn’t diligent. There can be other explanations, but, having read many of these rulings, I’ve not seen cases where an agent had valid mitigating circumstances that were overlooked by the regulator.

About 10-20% of cases are related to more serious infractions where harm was done to a client. Here we see:

· suitability violations (recommending something that was not appropriate);

· inappropriate use of leverage (having the client borrow without explaining the risks, or, in some cases, without understanding that they were borrowing);

· agents taking extreme measures to prevent clients from cancelling policies (including paying premiums, as I discussed here)

I encourage you to have a read of a few recent decisions at the national database. It’s a fascinating look into the world of insurance regulation. I’m often struck by just how small the fines levied in the insurance world are compared to what we see in the securities world, for example. Insurance regulation remains, in many ways, the Wild West of Canadian financial services.

Discussion