We're going to have a look at what the expectations and obligations are for an insurance agent who is placing a life insurance policy.

tl;dr: There is a very low bar for what the insurance agent is required to do.

This continues my series about insurance regulation and licensing, originating from this case where an agent sold 59 life insurance policies despite a lack of a license: https://teao.fsrao.ca/en/enforcement/2741?ref=fpcollective.ca

First, the Insurance Acts in all common-law jurisdictions are about a century old (Ontario was the first Canadian province to introduce an Insurance Act, in 1919. Other jurisdictions essentially copied this legislation over the next decade or so. Quebec, as in so many other things, did not take the exact same approach, and isn't dealt with in the scope of this article.)

That legislation was introduced at a time when the life insurance business was pretty simple. Agents had access primarily to whole life insurance, and a couple specialty products, including industrial insurance (a sort of precursor to group life, often sold in union shops) and funeral plans. Disability insurance was a simpler product than today, often sold as a component of a whole life plan, where a percentage of the whole life face amount was available as a monthly disability benefit.

Pretty much everybody selling insurance was a captive agent, selling the products of only one company. Agents who sold policies were given a 'receipt book'. Just as many policies were sold door-to-door, premiums on in-force policies were also paid door-to-door.

Insurance in those days was focused on the risks of premature death and disability. It wasn't until the 1950s and 1960s that we started to see retirement planning as a need, and this is where the evolution of the life insurance business from a pure product-sales business to a financial advisory business started. (We can see many of the same trends for securities licensees, who were originally stock-brokers in the traditional sense, but shifted to the delivery of financial advice based on a variety of market and regulatory trends.)

The result of these trends, then, is roughly that:

· Insurance agents have mostly become financial advisors, delivering advice that goes beyond just the products being sold.

· Product sales continue to be the sole or primary means of compensation for those agents.

· Insurance regulation and legislation has not changed meaningfully to reflect the shift away from product sales and to the delivery of financial advice.

There are some exceptions here. Saskatchewan has a robust Code of Conduct that includes suitability requirements for insurance agents.

The Canadian Council of Insurance Regulators, which has no direct regulatory authority, but is more of a working group for the provincial insurance regulators, has an ongoing project called Fair Treatment of Customers . The work done here informed the Saskatchewan Code of Conduct referred to above. Ontario has taken some steps in this direction, including the implementation of its Unfair and Deceptive Acts and Practices Rule. This rule is broad, and applies to the home and auto sectors as much as to the life insurance sectors.

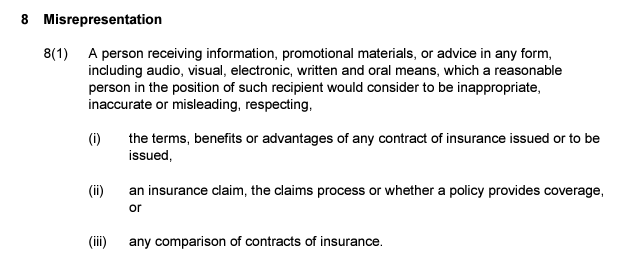

Even with these changes, the ability of insurance regulators to sanction agents is limited. The insurance regulator can really only sanction an agent for their specific activities with respect to an insurance contract. And those activities, outside of Saskatchewan, most likely, don't necessarily extend to any sort of effort to match the product to the client's need.

This means a client who is sold the wrong product (doesn't match their risk; a less expensive product with equal coverage was available; sold on tax merits that don't hold up to scrutiny) isn't necessarily left with much recourse. If, in Ontario, an agent used a deceptive comparison to support an insurance sale, that would be a violation of the UDAP referenced above, but this is a relatively new rule and the ability to use it as an enforcement tool hasn't been fully tested yet. Here is a recent case that does rely on UDAP, but for a fairly clear-cut violation, not for a suitability concern.

What about, then, an insurance agent who is delivering financial advice, and gives incorrect advice about a mortgage, credit building, or the rules concerning RRIFs? None of these are likely directly related to the insurance sale, meaning regulators are going to have a hard time enforcing any sort of sanctions. The client given this wrong advice may find some resolution in the courts, but this is a very time-consuming, emotionally-fraught, risky, and expensive way to resolve a problem.

I hope we see more provinces go in the direction of Saskatchewan, which at least has introduced a clear suitability requirement. Better yet, it would be nice to see some sort of regulation more broadly governing the delivery of financial advice. I hate to ask for more regulation, but the world has changed, and existing legislation and regulation has not changed with it.

As long as we continue to rely on outdated legislation, the bar for performance for those who carry an insurance license stays very low, and the requirements for consumers who have been harmed is very high. This creates a clear imbalance in favour of bad actors and hurts our industry.

Discussion