Insurance Crime Part II: Insurance Licensing

Continuing my series on FSRA's decision against an insurance agent who sold 59 policies despite a lack of an insurance license (https://teao.fsrao.ca/en/enforcement/2741) let's have a look at what an insurance agent's license means.

To get us started, we're going to do what nobody ever does, and read the Insurance Act. Each jurisdiction has its own Insurance Act, but they are, other than Quebec, quite similar from province to province to territory. We'll rely here on the Ontario Insurance Act, given that the offender in the case cited above was resident in Ontario.

The specific subsection of the legislation that was violated is:

Insurance agents normally have licenses that must be renewed every year or two (SK and ON both have two-year licenses):

The Insurance Act establishes very few requirements, obligations, and limitations on insurance agents:

- They cannot obtain insurance premiums via fraudulent means

- A person cannot hold out as an insurance agent unless they are one

- An insurer cannot remunerate an unlicensed person for placing or negotiating an insurance contract

It's the last point that is usually the reason for somebody to obtain an insurance license. Contrary to what I hear, the Insurance Act places no prohibition on delivering advice or anything else. The only prohibition is - you must be licensed to get paid for selling insurance policies.

The actual language is:

We can't just look at the legislation in isolation, though. Ontario, like most provinces, has regulation to augment and clarify what's in the legislation. In the case of Ontario, this is Regulation 347/04 - Agents.

This regulation sets a long list of criteria for somebody to meet to obtain an insurance license. These are mostly such broad principles that it would be hard to argue the finer points of them. For example, "is possessed of a reasonable educational background, if the applicant is an individual;" is one of the criteria, but with no further elaboration. I know plenty of insurance agents who have a high school education, and some who don't have that. (My own father came into the life insurance business in the early 80s with a Grade 10 education.)

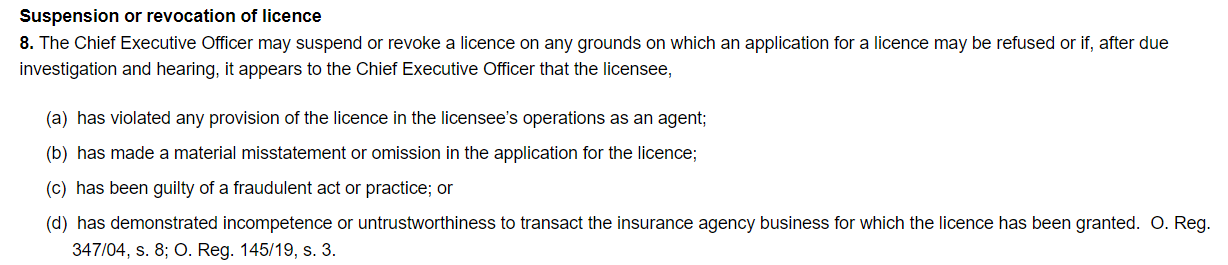

The powers granted to the insurance regulator in Ontario are detailed here as well, at S.8. Those powers basically allow FSRA to suspend or revoke an insurance license:

Because Ghuman acted as an agent despite not having a license, FSRA assessed him a $50,000 penalty. Said penalty is an administrative penalty, not a fine. Administrative penalties are attractive for regulators because they allow the regulator itself to administer a fine without having to go through the court system. They are typically used for 'minor' infractions, such as bylaw violations. There isn't any provision in the Insurance Act or Regulation for a regulator do do any more than levy administrative penalties and suspend a license.

In this sense, insurance legislation has effectively set up a 'victimless crime' scenario. No matter what the offender has done, they can likely escape consequences by simply leaving the business. It may not even be that difficult for that person to get licensed in another jurisdiction, as communications between provincial insurance regulators are not typically robust.

In a case like this, where the agent has done of the very few things explicitly proscribed by legislation, the consequences are effectively nil. Insurance legislation isn't set up to help consumers who have had harm done to them; it's set up to create a bare minimum set of rules so that insurers know the people acting as their agents have met at least a bare minimum set of standards.

Discussion